FIRE Calculator

Most people will work until they're 65. Not because the work demands it, but because nobody ever showed them the math.

There's a number that changes everything: the exact amount you need invested so your money covers your expenses forever. Every year you don't know it, you're trading time you'll never get back.

This FIRE calculator shows you that number — and exactly how many years until work becomes optional. Takes 30 seconds.

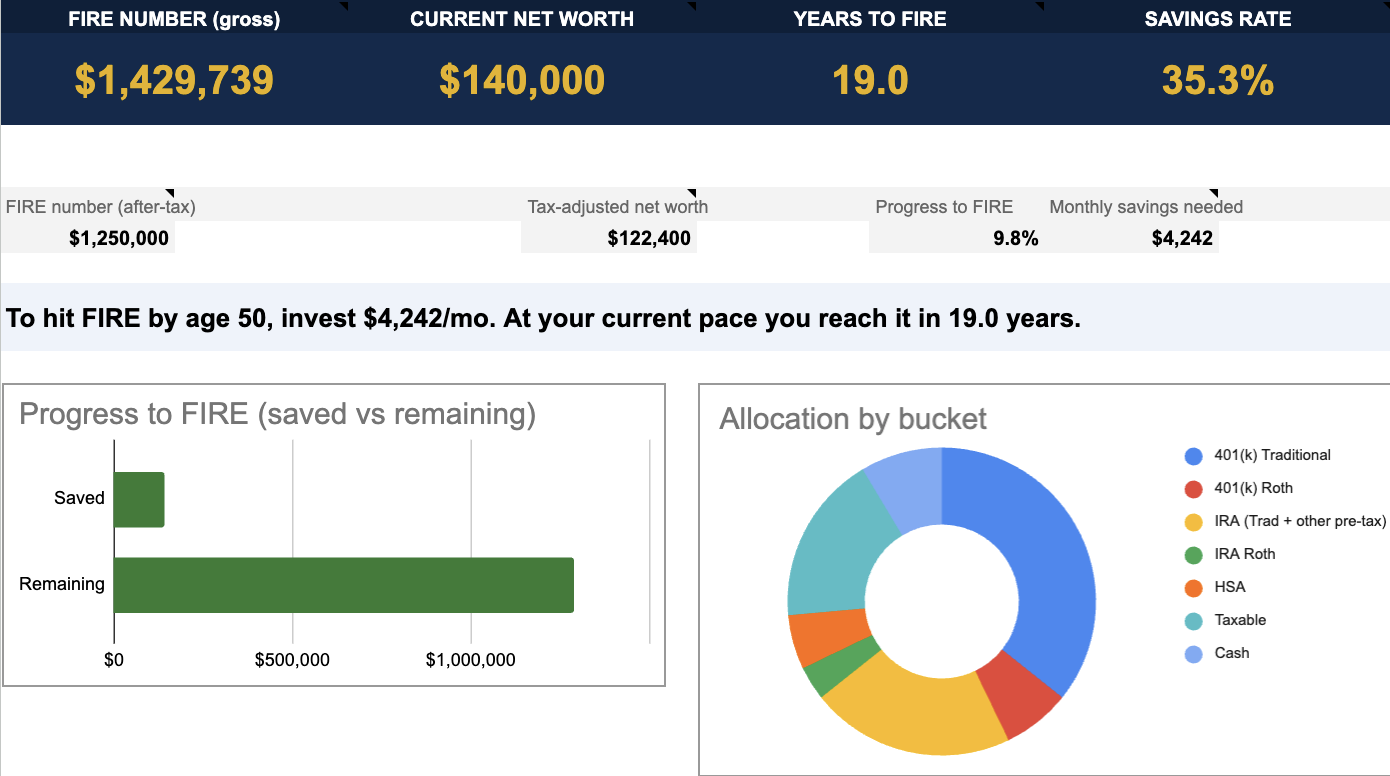

Your Results

Escape the 9-5 with FIRE

You just ran the numbers. The number is the easy part.

Most FIRE plans don't fail because the math was wrong. They fail in the gap between the number and the path: tax moves done in the wrong order, lifestyle creep that quietly resets the target, and One More Year Syndrome dragging the timeline five years past the day someone could have walked away. This book covers the path between the two, in 30 pages with no fluff.

- The savings rate table — see exactly how many years you can cut by saving 10% more

- Coast & Barista FIRE — the two paths most people overlook that get you out years earlier

- The Double Effect — why every spending cut does two jobs at once and why it beats a raise

- The tax stack — 401k → HSA → Roth Ladder, in the exact order that saves $20–50k over your career

- Sequence of returns risk — the timing problem that can wreck a perfect plan, and how to protect against it

- One More Year Syndrome — the trap that keeps people working five years past their number

- Plus the 2026 Tax Cheat Sheet — every contribution limit, bracket, and FIRE number on two pages, updated yearly

The calculator gives you the number. The book walks you through the moves that get you there.

Instant download — both PDFs.

FIRE Planning Workbook

You found your number. The Workbook shows you how to keep it through the tax maze.

Hitting your FIRE number is mostly arithmetic. The hard part starts the day you stop working and start withdrawing, because the order you pull money decides how much the IRS takes. The FIRE Planning Workbook takes your real numbers, your state, and your account mix, then runs the full US tax picture of your drawdown for every year of retirement. It's the Google Sheet you'd build yourself if you had a CPA and a free month.

- Tax-aware withdrawal tab — federal tax, cap-gains stacking, Social Security, MAGI, ACA exposure, IRMAA tier, and RMD for every year

- Six built-in calculators — Roth ladder, Rule 72(t) SEPP, 0% LTCG harvesting, ACA cliff, IRMAA projector, RMD

- Five-path scenarios — Lean, Regular, Fat, Coast, and Barista side by side, each with its own number and timeline

- Live dashboard, 50-year projection, and monthly net-worth tracker, all in today's dollars

- The 2026 Tax Cheat Sheet built in, with free updates through tax year 2030

Already read the ebook? This is the engine that runs those moves on your own numbers.

Instant access. Yours to copy and keep.

FIRE Calculator: find your number, then pick your path

Your FIRE number is the same no matter how you get there: annual spending divided by your withdrawal rate, or roughly 25× your yearly expenses at 4%. What changes is the route. This calculator runs the three most common ones so you can see which exit is closest.

Standard FIRE is full independence: a portfolio big enough that work is entirely optional. It's the biggest number and usually the longest road, and it's what this page opens on.

Coast FIRE is the point where you can stop saving entirely and let compounding finish the job by retirement age. It usually arrives years before full FIRE. Run it on the dedicated Coast FIRE calculator to see how much you need invested today to stop contributing.

Barista FIRE means semi-retiring now on a smaller portfolio, with part-time income covering part of your spending. The Barista FIRE calculator handles the part-time income and healthcare math. Want to retire on the leanest possible number, or the fattest? There's a Lean FIRE and Fat FIRE calculator too.

How the FIRE calculator works

This calculator uses the 4% safe withdrawal rule, the cornerstone of the FIRE movement. It was established by William Bengen in 1994 and confirmed by the Trinity Study: if you withdraw 4% of your portfolio in year one of retirement and adjust for inflation annually, your portfolio has historically survived 30+ years in 96% of scenarios.

Your FIRE number is your annual retirement spending divided by your withdrawal rate. At 4%, that's your annual expenses multiplied by 25. Once your invested portfolio reaches this number, you're financially independent and work becomes optional.

The calculator iterates year by year, growing your portfolio at the expected return and adding your annual savings, until it crosses your FIRE number.

Frequently asked questions

What is the FIRE number?

Your FIRE number is the total investment portfolio you need to retire early. It's your annual retirement expenses divided by your safe withdrawal rate. At 4%, your FIRE number is annual expenses × 25. If you spend $50,000/year, your FIRE number is $1,250,000.

What is the 4% rule?

The 4% rule states that you can safely withdraw 4% of your portfolio in year one of retirement, then adjust for inflation each year, with a high probability (around 96%) that your portfolio will last 30+ years. It was established by the 1994 Bengen study and confirmed by the 1998 Trinity Study. Some financial planners suggest 3.5% for early retirees planning for 40–50 year retirements.

What is Coast FIRE?

Coast FIRE means you have enough invested today that compound growth will carry your portfolio to your FIRE number by traditional retirement age, without adding another dollar. You can "coast" by working just enough to cover current expenses, with no need to save more for retirement.

What is Barista FIRE?

Barista FIRE means semi-retiring with part-time work that covers some of your expenses. Because your part-time income reduces how much you need from your portfolio, your required portfolio is much smaller. Every $1 of part-time income reduces your required portfolio by $25 (at 4% SWR). See the dedicated Barista FIRE calculator for the part-time income and healthcare math.

How much do I need to retire at 40?

To retire at 40, you need 25× your annual expenses (at 4% SWR). If you spend $50,000/year, you need $1,250,000. For a 50-year retirement, consider using 3.5% SWR instead, which works out to about 28.6× your expenses, or roughly $1,430,000 for $50K annual spending. The earlier you retire, the more conservative your withdrawal rate should be.

What return rate should I use?

The US stock market has returned approximately 10% annually before inflation (7% after inflation) over long historical periods. Most FIRE practitioners use 7% as a nominal return and 5% as a real (inflation-adjusted) return. This calculator uses nominal returns by default, so set it to 5% if you want inflation-adjusted projections.

Test your withdrawal rate

See how often a 4% (or any) withdrawal rate has historically survived your retirement length.

Open the SWR Calculator →