Safe Withdrawal Rate Calculator

Test any withdrawal rate against historical Trinity Study data. Adjust portfolio, allocation, and retirement length — see your success probability instantly.

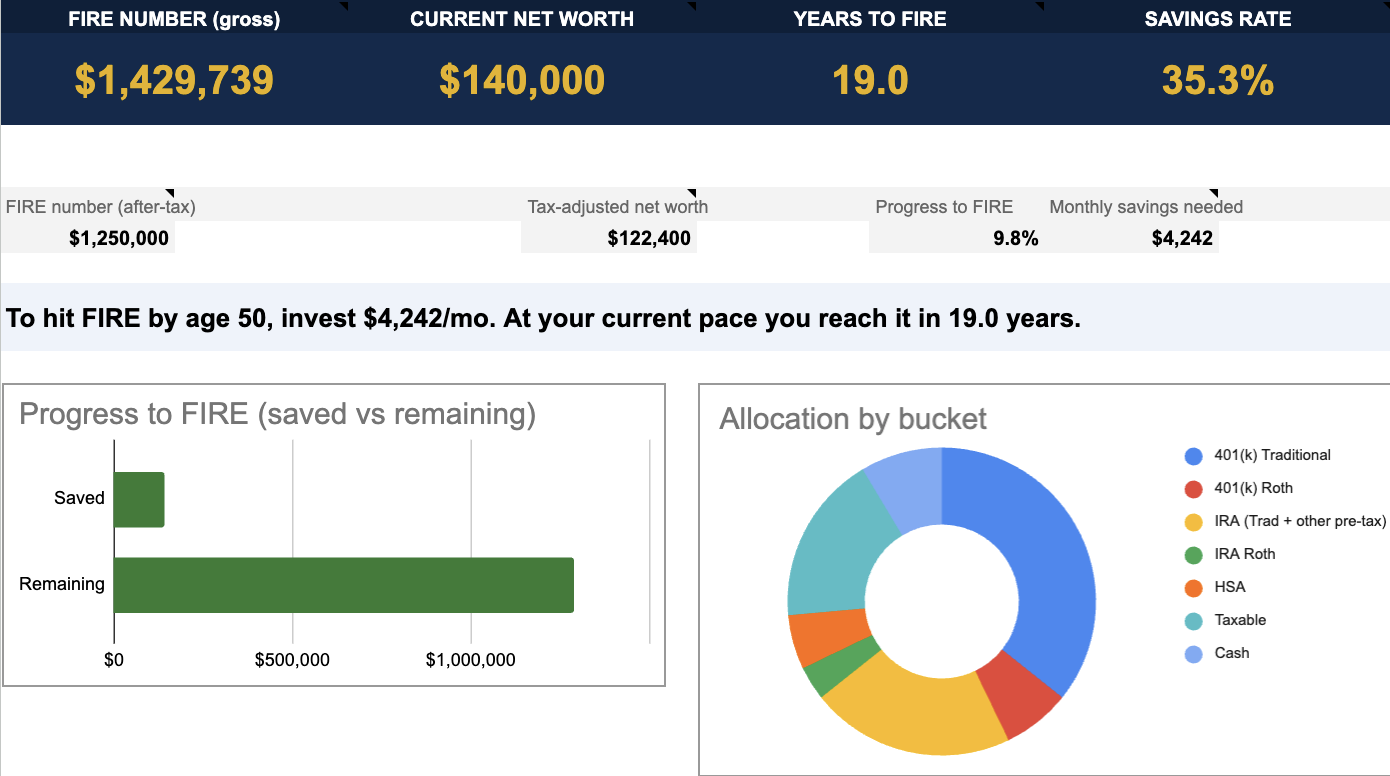

Escape the 9-5 with FIRE

You just saw a 100% success rate against history. The number you didn't see: 77 — the percent of your retirement's outcome decided in the first 10 years.

Trinity tested 30-year retirements through 2009. Yours runs 50 years through 2076, a different length and different starting valuations. In a 50-year retirement, sequence matters more than average returns: a sharp drawdown in years 2–3, combined with continued inflation-adjusted withdrawals, can shrink a portfolio that historically would have survived into one that doesn't. The calculator can't see this, because sequence risk is invisible to historical averages. The book covers the three moves that protect that first decade, in 30 pages with no fluff.

- Pfau's 3.5% argument — when the 4% rule still holds, when it doesn't, and how to decide for your specific horizon

- The first-decade rule — why 77% of your retirement outcome is decided in years 1–10, and the three concrete moves that protect it

- The guardrails strategy — why a 5%+ initial withdrawal with dynamic spending rules can be mathematically safer than a rigid 4%

- The Double Effect — why every spending cut does two jobs at once: more saved AND less needed

- The tax stack — 401k → HSA → Roth Ladder, in the exact order that saves $20–50k over your career

- Barista FIRE as sequence-risk insurance — why $10–20k/year of part-time income in years 1–10 does more mathematical work than almost anything else in early retirement

- One More Year Syndrome — the trap that keeps people working five years past their number, and how to recognize when you've crossed the line

- Plus the 2026 Tax Cheat Sheet — every contribution limit, bracket, and FIRE number on two pages, updated yearly

Trinity tested the past, and 4% won. Your retirement runs forward, for 50 years, through conditions that may not repeat. That gap, between historical confidence and forward planning, is what this book is for.

Instant download — both PDFs.

FIRE Planning Workbook

You tested the rate against history. Now run your actual withdrawals, year by year.

A success rate only measures whether a portfolio survives the years. What it leaves out is the tax you'll owe on the way out, and that is where early retirees quietly lose years of spending. The FIRE Planning Workbook takes your real numbers, your state, and your account mix, then runs the full US tax picture of your drawdown for every year of retirement. It's the Google Sheet you'd build yourself if you had a CPA and a free month.

- Tax-aware withdrawal tab — federal tax, cap-gains stacking, Social Security, MAGI, ACA exposure, IRMAA tier, and RMD for every year

- Six built-in calculators — Roth ladder, Rule 72(t) SEPP, 0% LTCG harvesting, ACA cliff, IRMAA projector, RMD

- Five-path scenarios — Lean, Regular, Fat, Coast, and Barista side by side, each with its own number and timeline

- Live dashboard, 50-year projection, and monthly net-worth tracker, all in today's dollars

- The 2026 Tax Cheat Sheet built in, with free updates through tax year 2030

Already read the ebook? This is the engine that runs those moves on your own numbers.

Instant access. Yours to copy and keep.

What is the Trinity Study?

The Trinity Study (Cooley, Hubbard & Walz, 1998, updated 2011) tested how often a hypothetical retiree's portfolio would survive a given withdrawal rate over various retirement lengths. Using rolling historical windows of US stock and bond returns from 1926 onward, the researchers computed the percentage of past 15-, 20-, 25-, and 30-year periods in which a retiree withdrawing a fixed inflation-adjusted amount each year did not run out of money.

Their headline finding: a portfolio of 50–75% stocks supporting a 4% initial withdrawal (adjusted annually for inflation) survived ~95–100% of historical 30-year retirements. This became the foundation of the "4% rule." This calculator looks up your inputs against the same data, capped at the 30-year horizon Cooley 2011 reports.

How to use this calculator

- Enter your portfolio value (or expected portfolio at retirement).

- Choose whether you want to enter your withdrawal as a dollar amount per year, or as a percentage of the portfolio.

- Pick your expected retirement length and stocks/bonds split.

- The success rate updates instantly. Withdrawals are assumed to be inflation-adjusted each year, exactly as the Trinity Study modeled.

Is the 4% rule still valid in 2026?

The original 4% rule has held up well historically, but recent research from Wade Pfau and others argues that today's lower expected returns (lower bond yields, higher equity valuations than the 1926–1995 average) make it more vulnerable. Pfau and others recommend 3.25–3.75% for new retirees with 30+ year horizons.

For early retirees facing 40–50 year horizons, sequence-of-returns risk becomes the dominant concern: a bad first decade can destroy a portfolio that would otherwise have survived. Many in the FIRE community now plan around 3.25–3.5% with the option to flex spending downward in bad years.

How allocation affects your success rate

Counter-intuitively, 100% bonds is one of the worst allocations for long retirements at any meaningful withdrawal rate. Bond returns over multi-decade windows have not kept up with inflation reliably enough to support sustained withdrawals. 100% stocks, despite higher volatility, has historically produced the highest long-horizon success rates above 4%, though with much wider drawdowns. The classic 50/50 to 75/25 split balances these forces.

Frequently Asked Questions

What's a safe withdrawal rate?

A "safe" withdrawal rate is the percentage of your portfolio you can withdraw in year one of retirement, then adjust annually for inflation, with high historical confidence (typically 95%+) that your portfolio will outlast your retirement. The Trinity Study suggested 4% for 30-year horizons in 50/50 to 75/25 allocations; modern research often suggests lower for early retirees.

Does this account for taxes?

No. The Trinity Study and this calculator use gross (pre-tax) withdrawal amounts. You should add an estimate for federal/state taxes to your annual spending before entering it.

What about Social Security?

Social Security and other pension income are not modeled here. If you'll receive them later in retirement, your portfolio only needs to cover the gap between spending and other income. Use a separate calculator for that planning.

Why do longer horizons need lower withdrawal rates?

More years means more chances for a bad market sequence early in retirement, which can permanently shrink the portfolio. Longer horizons also amplify the cumulative drag of inflation. A 50-year retirement may require 3.0–3.5% versus 4% for a 30-year retirement.

Should I use 4% or 3.5%?

For traditional 30-year retirements with a balanced portfolio, 4% has strong historical support. For 40+ year early-retirement horizons, or for retirees uncomfortable with sequence risk, 3.25–3.5% is more conservative and reflects current research.

What's the difference between the Trinity Study and Monte Carlo?

The Trinity Study uses historical rolling windows, every actual 30-year retirement period in the data. Monte Carlo simulations generate thousands of synthetic return sequences from statistical distributions. Trinity is more conservative and grounded in real history; Monte Carlo can model scenarios that haven't happened yet but is sensitive to the assumed return distribution.

Can I use this for non-USD portfolios?

The data is based on US stock and bond returns. For other currencies or non-US portfolios, the results are directional but not precise. Local equivalents (e.g., research on UK or Norwegian historical returns) would be more accurate.